VAR / SVAR / TVP-VAR in R (IRF / FEVD)

I build robust pipelines for VAR, SVAR, and TVP-VAR in R, covering model specification, estimation, and clear interpretation of results for coursework, projects, and research. I am fluent with the R ecosystem (vars, svars, bvar, tvReg/FKF, tsDyn) and deliver clean, reproducible scripts and figures suitable for reports or theses.

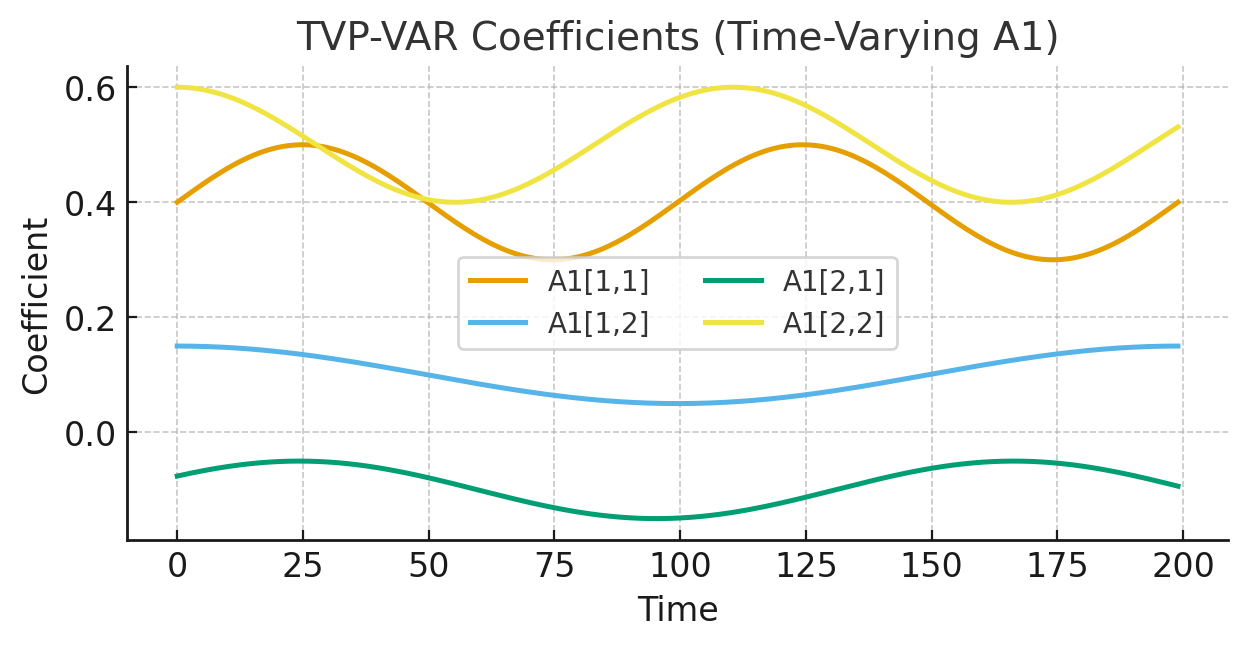

Model classes & options: reduced-form VAR(p); cointegrated systems (VECM/Johansen) with transformation to VAR; structural VAR identification (short-run zero restrictions, long-run Blanchard–Quah, sign restrictions, narrative/IV/Proxy-SVAR); Bayesian VAR (Minnesota/SSVS/shrinkage); time-varying parameter VAR (TVP-VAR) with stochastic volatility or constant variance; Markov-switching VAR; conditional/partial VAR; exogenous controls (VARX), deterministic terms (trend, seasonal dummies), and small-open-economy blocks.

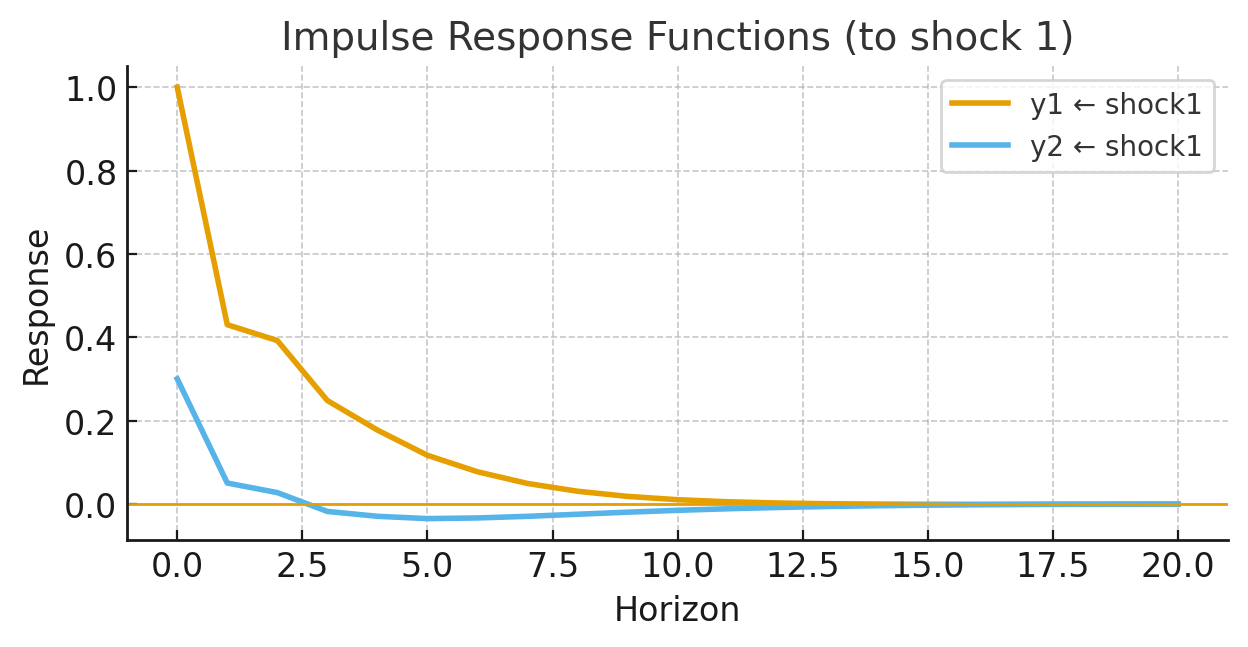

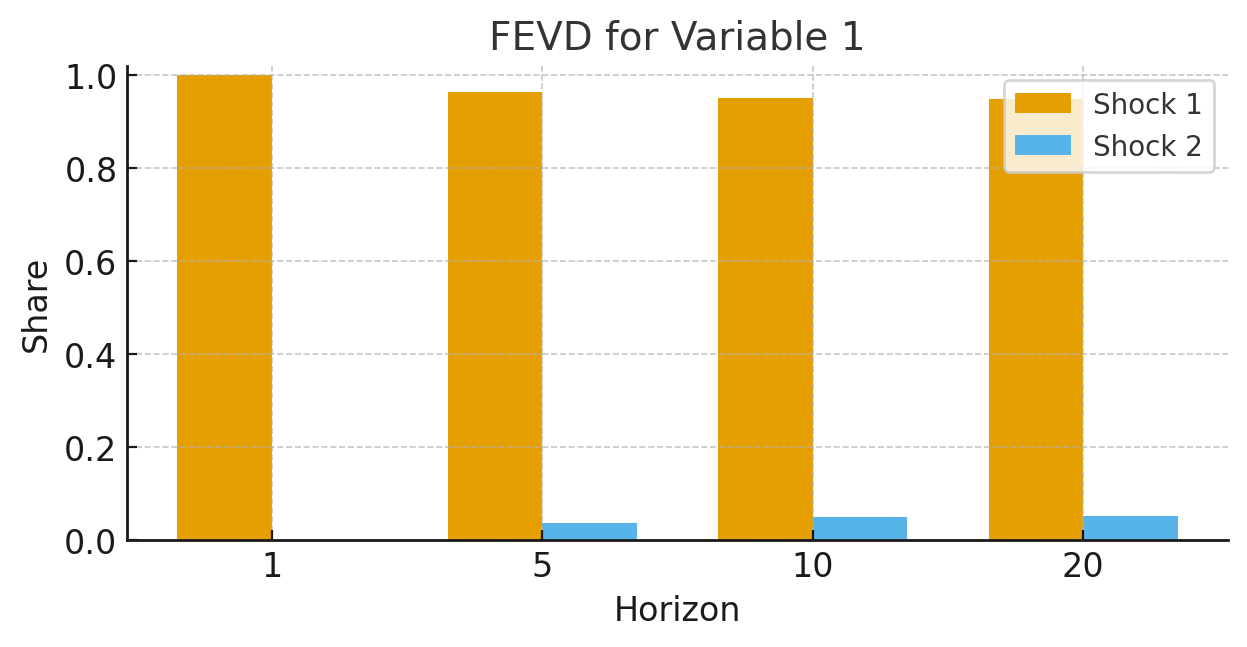

Identification & inference: Cholesky (recursive) ordering, long-run restrictions, sign/zero matrices, external instruments, penalty/median-target approaches, heteroskedasticity-based identification, and bootstrapped or Bayesian credible bands for impulse responses (IRF) and forecast error variance decomposition (FEVD). I provide cumulated/level IRFs, horizon-by-horizon FEVD tables, historical decompositions, counterfactuals, and conditional forecasts.

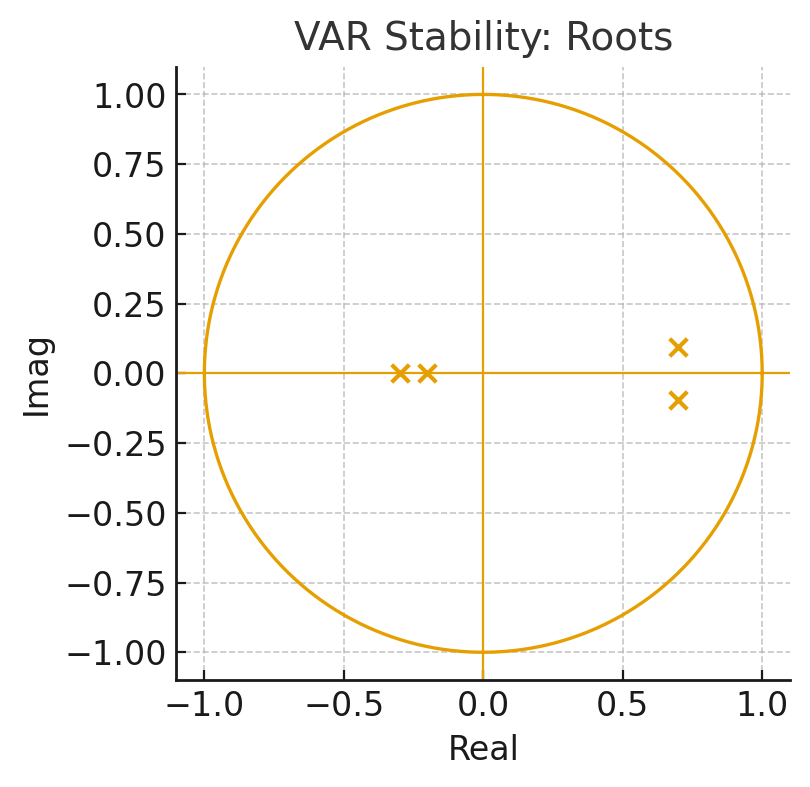

Diagnostics & validation: lag-length by AIC/BIC/HQ; stability (companion-matrix roots); LM/Portmanteau tests for residual serial correlation; normality and ARCH effects; structural break tests; parameter/sign-restriction sensitivity; small-sample and wild/bootstrap procedures; rolling/recursive evaluation and out-of-sample forecast accuracy.

Deliverables & support: well-commented R scripts, publication-ready IRF/FEVD/stability figures, concise interpretation notes, and optional write-up text. I can tailor the workflow to your dataset and research design and assist with replication, robustness sections, and presentation slides.

Engagements start at USD $150 with fixed quotes after I review your brief and data. I am familiar with these methods and can provide hands-on help in R programming end-to-end.