ARDL / NARDL — Bounds Testing, Long-Run & Asymmetry in R

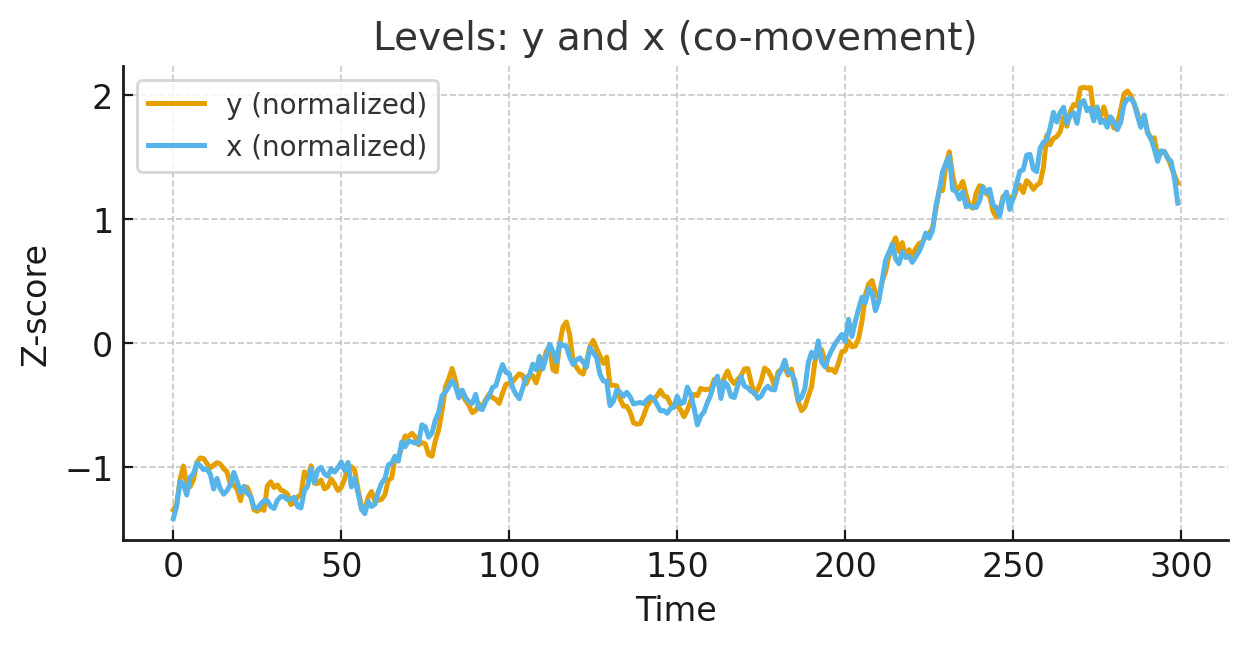

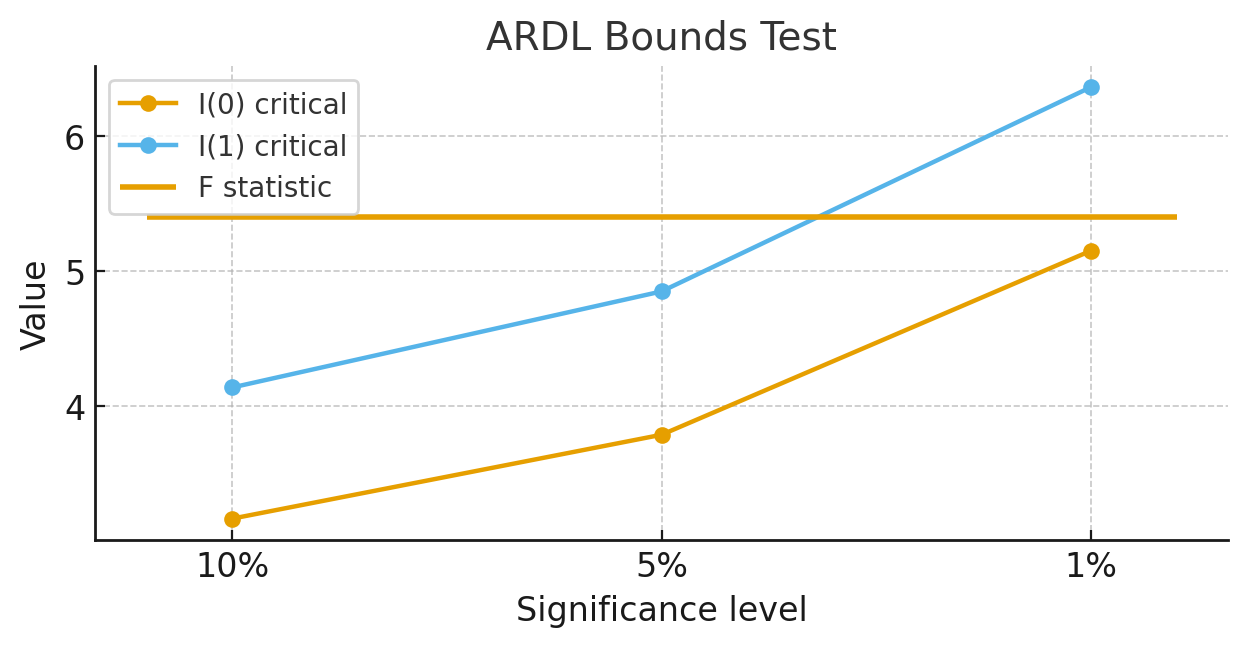

I implement ARDL and NARDL workflows in R—from identification to inference—tailored to coursework, projects, and research. I’m familiar with all key steps: transforming an ARDL(p,q) into the UECM, performing the PSS bounds test for level relationships, and recovering long-run coefficients and the error-correction term (ECT) when cointegration is present.

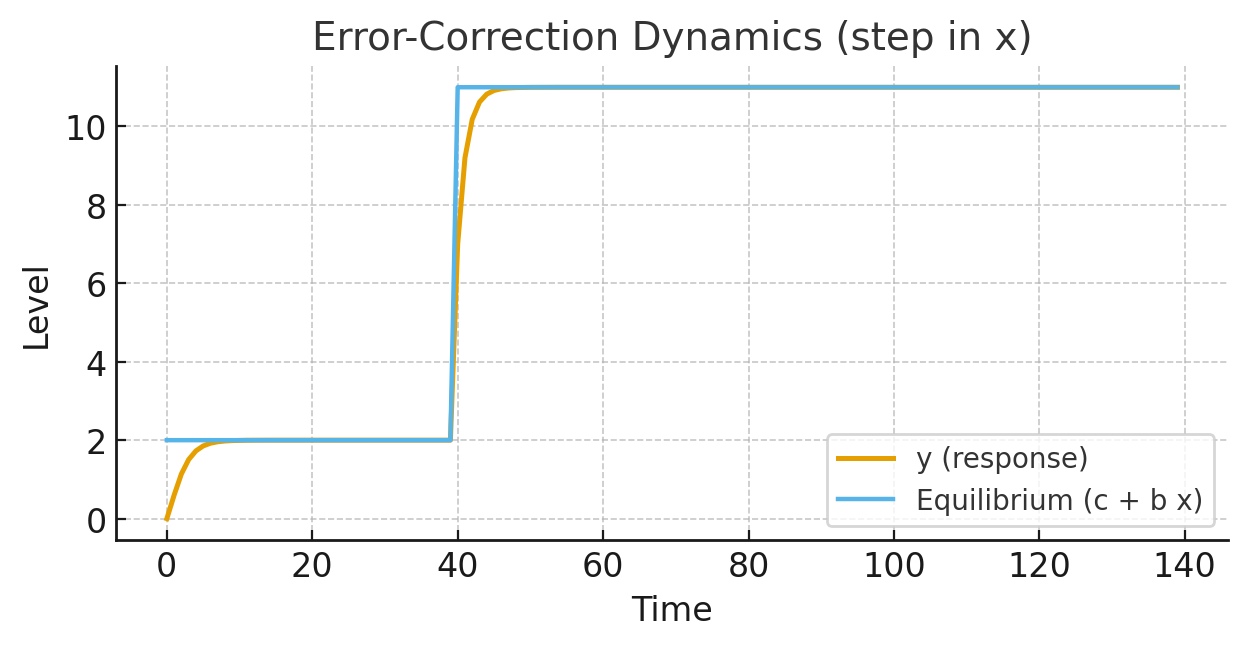

Core methods: ARDL(p,q,…), ARDL-ECM specification; lag-order selection via AIC/BIC/HQ; deterministic components (constant, trend, seasonals); exogenous controls; structural breaks and intervention dummies; short-run dynamics and long-run multipliers; dynamic forecasts and impulse/step responses; multi-horizon accuracy and rolling evaluation.

Diagnostics & validation: residual serial correlation (BG/Portmanteau), Breusch–Pagan/White tests, normality checks, stability (CUSUM/CUSUMSQ), RESET/specification, parameter significance, and small-sample robust inference (bootstrap where appropriate). I also report bounds critical values, ECT magnitude (speed of adjustment), and long-run elasticity interpretation with confidence bands.

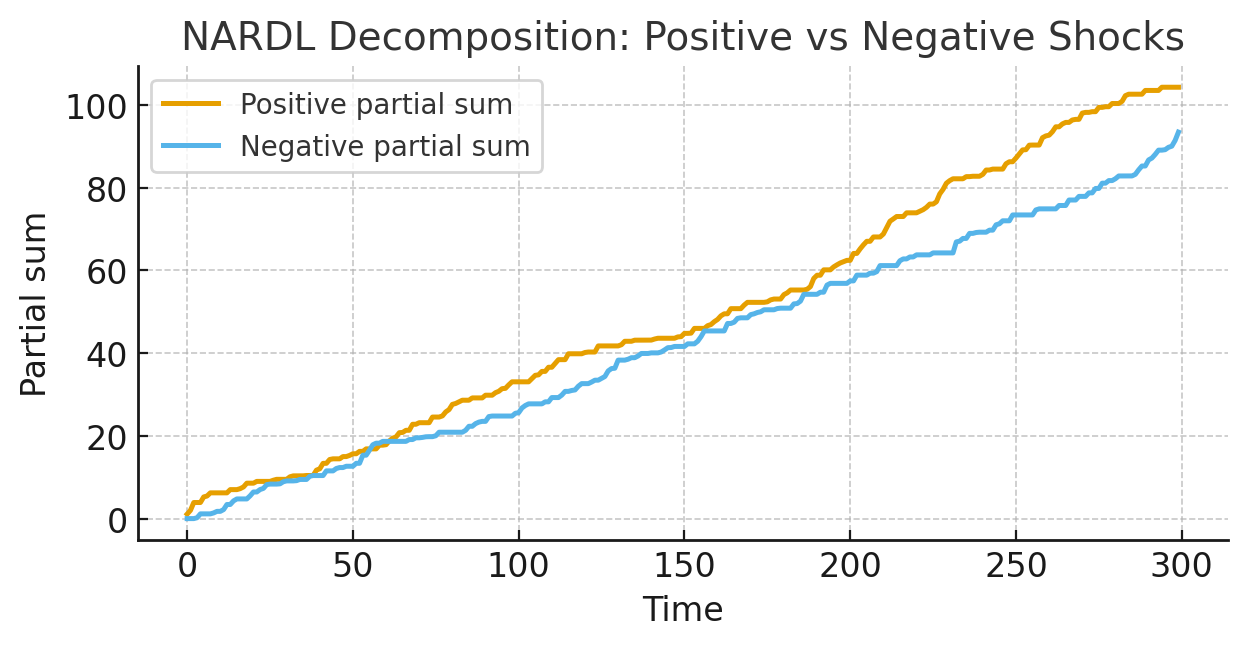

NARDL (asymmetry): partial-sum decomposition of positive/negative changes, long-run and short-run Wald tests for asymmetry, and dynamic multipliers tracing the effects of up/down shocks separately. Extensions include multiple regressors, threshold interactions, and out-of-sample forecast comparison with ARIMA/ETS.

Deliverables: clean R scripts, publication-ready figures, and concise interpretation you can insert into reports or theses. I am very familiar with these methods and can provide hands-on R programming help end-to-end.

Get help: engagements start at USD $150; fixed quotes follow a brief review of your data and scope.